Part 2 of a two-part series. Part 1, published last week, mapped the four-stage cycle of vendor lock-in.

Disclosure: I have had discussions with Airwallet as a potential secondary payment system at my laundromat. That conversation is how I first became aware that flat-fee monthly pricing exists in our industry, and it came about from me exploring other payment methods. As of the writing of this editorial, I have no signed agreement with Airwallet. The model described here is based on Airwallet's publicly available pricing structure. Airwallet has not paid, sponsored, reviewed, or otherwise contributed to this editorial. They are named because their pricing model is the structural alternative the piece examines.

On Friday afternoon, after thinking all week about how to lift weekend revenue, an owner/operator I know decided he would hand out flyers. He designed them himself that night. Saturday morning, before sunrise, he started walking the neighborhood his store is in. He kept walking Sunday too. By Sunday night, his weekend revenue was up twenty-two percent over the previous weekend.

He printed the flyers. He used his own gas. He gave up a weekend.

The share of that lifted revenue that ran on cards moved through a chain of vendors who took their proportional cut. None of those vendors walked the blocks. None of them designed the flyers. The structure of the relationship made their share rise as his did.

That is the question Part 2 is about. What does the vendor have to do to earn the increase, and what happens to a business when the answer is nothing?

Where We Left Off Last Week

In Part 1 of this two-part series last week, the editorial examined the four-stage cycle that economists Joseph Farrell and Paul Klemperer described in 2007. The owner/operator adopts a vendor. The owner/operator builds the business around the vendor. The vendor consolidates. The vendor restructures the relationship. By the fourth stage, the owner/operator faces a math problem, pay the new price or replace tens of thousands of dollars of equipment and retrain everyone who interacts with it.

That cycle is vendor lock-in. Today's editorial examines what lives inside the lock-in for a laundry business, the financial structure that quietly converts your business growth into someone else's revenue.

The Mechanics of a Card Transaction

Owner/operators sign agreements with terms like interchange, assessment, and processor markup printed on them. Some never get to see the full breakdown of what those terms mean in actual dollars. So I’ll do my best here to break it down.

When a client uses a credit or debit card to start a machine or load funds onto a laundry card, four parties are involved in the transaction. The bank that issued the client's card, called the issuer (Chase, Capital One, Bank of America, and so on). The card network, typically Visa, Mastercard, Discover, or American Express. The merchant's processor, which is the company actually moving the money. And the merchant.

Three real costs are paid in any transaction.

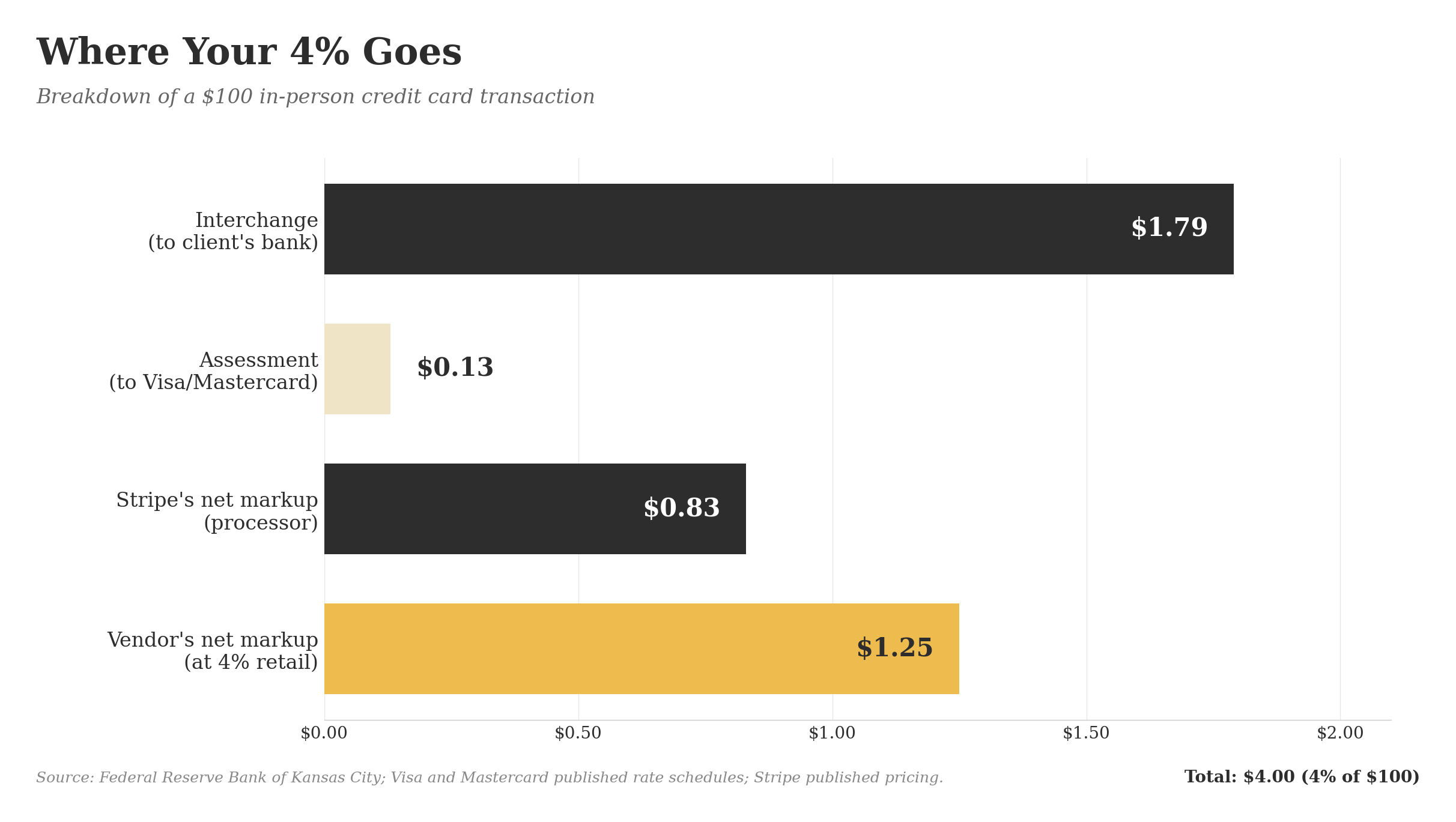

The first is interchange, paid to the bank that issued the client's card. Interchange compensates the issuing bank for taking on the risk of fronting the money to the merchant before the cardholder pays their statement, and for funding the cardholder's rewards program. It is set by the card network and varies by card type and merchant category. The US average across all credit card transactions is approximately 1.79%.¹

The second is the assessment, paid to the card network itself (Visa, Mastercard, etc.). This is the smallest of the three. It runs 0.11% on most transactions and 0.13% on transactions of one thousand dollars or more.²

The third is the processor markup. This is the layer where the processor's own profit lives. It is also where every payment vendor downstream of the processor adds its own markup on top.

Here is how that breakdown works in dollars, using Stripe's published pricing as a working example.

Stripe charges 2.9% plus thirty cents per online transaction and 2.7% plus five cents per in-person transaction.³ Those rates already include interchange, the network assessment, and Stripe's own markup, bundled into a single number for the merchant.⁴

Take a $100 in-person credit card transaction. Stripe collects $2.75 from the merchant on that transaction. Inside that $2.75, approximately $1.79 goes to the bank that issued the client's card as interchange. Approximately $0.13 goes to Visa or Mastercard as the assessment. Stripe's net markup is approximately $0.83.

Now apply that to when a laundry payment vendor charges the operator a 4% processing fee, the math is publicly testable. On that same $100 in-person transaction, the vendor charges the operator $4.00. The vendor pays Stripe $2.75. The vendor's net is $1.25 per $100 transaction, approximately 1.25% of every dollar processed. That $1.25 is not the cost of running the transaction. That is what the vendor makes on it.

When platforms describe their pricing as competitive, the breakdown above is what makes that claim testable. With the components visible, an operator can run the math themselves on the back of a napkin.

When the Percentage Compounds

The percentage is not the story by itself. The structure of the percentage is.

The math holds at any percentage. A vendor at 1.5% has the same structural relationship to operator growth as a vendor at 4%. The shape of the relationship is the same. Only the slope changes.

Imagine a store opens in week one and processes $5,000 in card revenue from self-service. At a 4% processing fee, the chain of vendors collects $200 that week. Four weeks later, the same store is processing $10,000 in card revenue. The chain of vendors collects $400 that week.

Their revenue from that store doubled in four weeks.

What changed on the operator's side, opening costs, marketing, staffing, operational attention, equipment depreciation, the gas in the operator's car, the operator's time. What changed on the vendor's side, nothing material. The same hardware sits on the same machines. The same software runs in the same data center. The same support team handles the same volume of tickets, distributed across thousands of other accounts.

The principle holds at every scale of growth. The flyer-driven 22% over a weekend. The 8% lift that comes from a strong year at a different store. The 50% jump from a renovation and relaunch at a third store. In each case, the percentage take rises with the revenue. The cost to serve does not.

Every dollar of growth the operator produces, produces growth for someone whose work has not scaled with the operator's.

Examining the Vendor's Position

Vendors have a real position here. They invest in research and development. They run support teams. They maintain infrastructure. They handle compliance. None of that is free.

Those costs are real. The question is whether they scale with any single operator's revenue.

A processor's research and development cost is amortized across its entire customer base. The variable cost of running one more transaction through existing infrastructure is small relative to the percentage charged on that transaction. Support, infrastructure, and compliance are similarly fixed against scale, not against the individual account. When an operator grows from $5,000 a week in card revenue to $10,000 a week, the vendor's actual cost to serve that operator does not double. The percentage payment does. That is the structure.

There is also an industry-specific observation worth making. Several laundry payment and POS platforms have added geofencing to their pickup-and-delivery offerings in the past couple of years. Geofencing is the technology that lets a delivery service draw a shape on a map and define what falls inside it. Uber launched in 2010 using geofencing-based dispatch from day one.⁵ By the mid-2010s, geofencing was a standard feature in major consumer logistics apps.

Back in 2016, when we started exploring pickup-and-delivery and were searching for a platform, only one or two had geofencing. The technology was already standard in every consumer app I used personally. The laundry industry caught up to it across the next decade.

That is not a failure. Catch-up is part of how every industry that lags consumer technology eventually modernizes. But it is worth naming for what it is. When the R&D defense for percentage-based pricing rests on innovation, the question becomes, innovation against what frontier? In industries with genuine technical frontiers, the defense holds. In commercial laundry, much of what has shipped after years of percentage-based revenue has been catch-up to consumer technology a decade old. The defense is real. The bandwidth for it is narrower than the framing suggests.

The Same Pattern, In Other Industries

This is not a laundry pattern. It is a pattern in how percentage-based vendor relationships behave generally.

Etsy, 2022. Etsy raised its seller transaction fee from 5% to 6.5%, a 30% increase.⁶ The mechanism that drew protest from sellers was the same one we are examining here: a fee that scales with seller revenue, applied across millions of sellers, where the platform's cost to serve any individual seller did not change with the fee increase. The structural argument has been the same in seller forums for years.

Restaurant delivery apps. DoorDash's commissions to restaurants run 15% at the basic tier, 25% at the next tier, and 30% at the top tier.⁷ Uber Eats raised its Lite tier from 15% to 20% earlier this year.⁸ Industry-average restaurant net profit margin runs around 15%.⁹ The structural observation: percentage pricing on a service relationship can grow large enough relative to operator margin that the operator does the work and the platform earns the money.

Shopify. Subscription tiers run from $39 to $399 per month for standard plans, plus 2.4–2.9% and thirty cents per transaction in payment processing, plus an additional 0.2–2.0% surcharge for using a non-Shopify processor.¹⁰ A pricing analysis by SBI Growth found that scaling credit card rates and percentage transaction fees account for close to half of Shopify's overall revenue.¹¹ The structural observation: even when a vendor charges a flat subscription, the percentage layer can be where the larger revenue is built. The subscription is not always the relationship. The percentage often is.

Real estate. A real estate agent who sells a $300,000 home and a real estate agent who sells a $1,000,000 home do substantially the same work. At a 5% commission, the second agent earns more than three times what the first one does. The structural observation: percentage pricing rewards the size of the underlying transaction, not the work that produced it. Most homeowners have personally felt this math.

Marketing services in our own industry. A laundromat owner/operator hires an SEO firm or a Google Ads management firm. The firm typically charges a flat monthly management fee plus a separate ad budget. If the ads produce $30,000 in new business that month, the firm earns the same management fee. If the ads produce $300, same fee. The vendor's revenue is tied to the work the vendor has done, not to the size of the result. Most laundry owner/operators have a vendor relationship structured this way today. The structure is not impossible. It just has not been the default in payment processing.

The pattern across the first four cases is consistent, percentage scales with the operator's revenue, vendor work does not. The fifth case shows the alternative structure already exists in our own industry, applied to a different category of vendor.

Another Pricing Structure

When a fee is tied to revenue, growth pays the vendor. When a fee is flat, growth pays the operator. That is the structural difference.

There is also a middle position worth naming. Even within percentage pricing, the math itself suggests the rate should decline as operator revenue grows, because the vendor's marginal cost on each additional transaction is small relative to the percentage charged. A vendor whose rate stepped down at higher revenue tiers would still earn more from larger operators than from smaller ones, just less disproportionately so. That structure is uncommon in the laundry industry. The default sits at the more extractive end of the spectrum, a constant percentage that scales linearly with operator revenue regardless of size.

Why has the constant percentage become the default in our industry? Why has there been no mainstream sliding-scale option, no widely available flat-fee option until recently? The question is not academic. A flat-fee model exists, today, in laundry industry, Air Wallet charges owner/operators a fixed monthly fee per device. The exact wording from their website and materials: *"With Airwallet you pay a fixed monthly subscription fee. There are no additional transaction fees or service costs, everything is already included, so you always know what to expect."*¹²

Their support documentation puts it more directly, *"Subscription prices already include all transaction fees and provisions, so no additional payments are required."*¹³

What is notable is not that the alternative exists. It is that percentage pricing has been the default in our industry for so long that the alternative looks unusual, but viable.

What the Structure Reflects

A vendor can be excellent at hardware. Excellent at software. Excellent at support. The fee structure can still be the wrong part of the relationship.

That is a different argument than fees being too high. Fees being too high is a complaint about a number. The structure of the relationship is a question about how the relationship is designed.

As costs and pressures rise across the laundry business, the question worth asking about every recurring vendor relationship is whether the structure is equitable. Whether the vendor's revenue scales with work the vendor has actually done, or with work the operator has done.

When the operator hands out flyers Saturday and weekend revenue lifts 22%, the only party who did the work to produce that 22% is the operator. The vendor's claim on the share that ran on cards is structural. It was written into the contract on day one, before any flyer existed.

The structure is a choice. It was a choice when the contract was signed. It remains a choice every time the operator looks at a vendor relationship and asks what kind of partner this actually is.

Thinking about the thinking of laundry:

Once you can see inside the processing fee, the question stops being how much you're paying and starts being why the math compounds for someone whose work hasn't.

That's all I got for you today.

Waleed

Echoing the thoughts of Charlie Munger.

Show me the incentive and I will show you the outcome.

² Visa and Mastercard Assessment Fees — published rate schedules

³ Stripe Pricing — Stripe official pricing page

⁴ How Stripe's Bundled Pricing Works — Stripe Documentation

⁵ Geofencing in Modern Consumer Apps — overview of mid-2010s consumer tech adoption

⁶ Etsy Sellers Strike Over Fee Increase — NPR, April 11, 2022

⁷ DoorDash Commission Tiers for Restaurants — Sauce, April 2026

⁸ Uber Eats Raises Commission Rates — Prism News, April 2026

⁹ Industry Average Restaurant Profit Margin — CloudKitchens / Toast industry data

¹⁰ Shopify Pricing Plans 2026 — Shopify official pricing page

¹¹ Shopify's Smart Pricing Strategy — SBI Growth pricing teardown

¹² Airwallet Owner Pricing Information — Airwallet

¹³ Airwallet Subscription and Billing — Airwallet WISER documentation