I need to share with you something that happened the other month.

We were working with a credit card processor who would integrate with our card system and charge less than half of the 4% we'd been locked into.

We got it set up. Everything worked. Then the card system provider for our washers and dryers, the system clients use to start the machines updated their software.

The integration stopped working. Not just for us, but for other stores using that processor too. When the processor reached out to resolve it, they were told, "We only work with one processor." No technical explanation. No security concern. Just blocked.

Now we're back to paying 4%. And we're not alone.

The Franchise Nobody Signed Up For

At the Laundry CEO Forum, I kept hearing similar stories from owners/operators, I have heard before and seen in online groups, "My processing fees are too high," "I'm trying to negotiate lower rates, with no luck.”

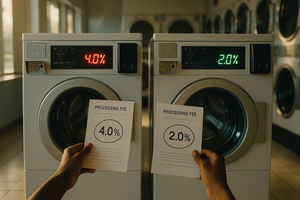

Others have shared their paying up to 4% on their card system for washers and dryers. 4% on their POS system for products, wash-and-fold, and pickup-and-delivery. Some owner/operators are paying processing fees on every revenue stream in their business.

Think about what you get when you pay 4-8% to an actual franchise:

- ✅ Brand recognition

- ✅ Marketing support

- ✅ Training systems

- ✅ Collective buying power

- ✅ Operational playbooks

- ✅ And more.

Now think about what you get when you pay 4% to a payment processor:

- ✅ The ability to accept credit cards

That's it. You're paying franchise level fees for a utility service.

The Small Business Squeeze

This isn't just a laundry problem. Credit card processing fees have become the third-largest expense for small retailers, right behind rent and payroll.¹ That’s mind blowing.

In 2023, merchants paid $172 billion in processing fees, a 48% jump from pre-pandemic levels.² These fees are outpacing inflation while small businesses lack the bargaining power that large chains use to negotiate lower rates.³

Standard processing rates for most retail businesses run 1.5-2.5%.⁴ So why are laundry business owners/operators paying higher rates, and in some cases, 4%?

I believe part of it comes down to: proprietary lock-in, little to zero negotiating leverage, and limited choices in our industry.

The Lock-In Problem

Here's what makes the laundry industry different.

Installing a card system isn't cheap. Depending on store size, you're looking at $20,000 to $50,000+ for the vending machines that dispense cards, takes credit/debit card payment and collect cash, plus readers on every washer and dryer. And if you have ancillary equipment like vending machines or want to take card payments at your POS counter, you'll need readers for those too.

That's a massive investment. Which means when you discover you're paying double the standard processing rate, switching isn't as simple as "find a better deal."

Not all providers operate the same way. Some card system and POS providers give you real options, and these are the ones doing it to the benefit of the laundry business. They let you choose from multiple processors, bring your own, or they've already negotiated competitive rates in the 2% or lower range with their single processor. This is what client first practice looks like.

Others lock you in. One processor. Non-negotiable. And if you're a solo operator or running 1-2 locations, you have almost no leverage to negotiate. Even at 3+ locations, your bargaining power is limited compared to chains running 10+ stores.

The operators who successfully negotiate lower rates? They typically have multiple locations and use that volume as leverage. The rest pay whatever rate they're given.

What This Actually Costs

Let's look at one laundromat volume example:

Single Location:

- Self-service revenue (card system): $12,000/week

- POS counter (products + WNF + PUD): $6,000/week

- Total weekly card transactions: $18,000

At 4% processing fees:

- Weekly: $720

- Monthly: $3,120

- Yearly: $37,440

At 2% processing fees:

- Weekly: $360

- Monthly: $1,560

- Yearly: $18,720

The difference: $18,720 per year. That's a significant chunk of equipment maintenance, payroll, marketing budget, or profit you actually keep.

Now scale it:

3 locations at the same volume:

- 4% fees: $112,320/year

- 2% fees: $56,160/year

- You're transferring $56,160 annually to processors

5 locations:

- 4% fees: $187,200/year

- 2% fees: $93,600/year

- You're transferring $93,600 annually to processors

Over 10 years at 5 locations: $936,000 that could have stayed in your business went to payment processors instead.

The Irony Nobody Mentions

You know who doesn't have this problem? Operators still running on coins.

They have other challenges. Security concerns. Logistics of collecting and counting. Scaling difficulties across multiple locations. But they're not paying a 4% tax on every transaction.

The "modernization" that was supposed to make business easier is costing some owner/operators double what it should. When the technology meant to improve efficiency becomes one of your largest expenses, something's wrong.

What to Do About It

If you haven't bought a system yet, ask these questions:

- Can I choose my own processor?

- What are the actual processing rates?

- Can I bring my own processor if I find better rates?

- What does it cost to switch if I leave?

- What's the best rate you can do for me?

- Can you break down interchange fees vs your markup vs per-transaction fees?

- Will you match my current processor's rate if it's lower?

- Are your rates competitive with general retail, not just laundry?

Don't assume all providers are the same. Some offer transparency and choice. Others lock you in and profit from the difference between what they pay processors and what they charge you.

If you're already locked in:

Individual operators with 1-2 locations have limited leverage. But collective action works. Find other operators using the same platform. Band together. Approach the provider as a group and discuss better rates.

You'd be surprised what happens when 5-10 operators collectively say “lets negotiate better rates."

For the industry:

Platforms should disclose processing fees upfront on their websites, not make them an afterthought or secondary consideration. Fees should be listed prominently alongside features.

Look at what Square did when they entered the retail payment processing market. They put their rates right on their website: 2.6% + 10¢ per transaction. No contracts. No lock-in. Complete transparency before you buy or even contact them for a demo.⁵

A couple of laundry providers do list their processing rates on their websites. But some don't.

Equipment should work with multiple processors, not create artificial lock-in. And owners/operators deserve transparency about what portion of their fees goes to actual processing versus platform profit.

Thinking about the thinking of laundry:

When you realize you’re paying franchise level fees without getting franchise benefits, you're not modernizing your business, you're subsidizing someone else's.

Next Steps This Week:

- Pull your last three months of processing statements

- Calculate what you're actually paying in fees as a percentage

- Connect with other owners/operators using the same system and have open dialogue to see what they're paying versus what you're paying

- Reach out to your provider and ask for a better rate

- Start a conversation about collective negotiation with other operators if you can't make headway on your own

In a world where profit margins matter and every dollar counts, paying double the standard processing rate isn't "just the cost of doing business." It's a choice. And now you know there are options.

That's all I got for you today.

Waleed

PS: Building something for laundry entrepreneurs who want real discussions without the noise. Early access: joinpressed.com

Echoing the thoughts of Waleed Cope.

When the people selling you the tools profit more from your transactions than you do, you're not a client—you're the product.

Share these insights

Did you enjoy this editorial? Forward it to colleagues and friends so they can subscribe too. Was this issue forwarded to you? Sign up for it here.

Footnotes:

¹ KSBY, "Small Businesses Feeling the Pinch of Rising Credit Card Fees," 2024

² New York Times, "Swipe Fees and Merchants," November 2024

³ NFIB, "Small Businesses Need Credit Card Swipe Fee Reform," 2024

⁴ SwipeSum, "The True Cost of Credit Card Processing in 2025: A Merchant's Guide"

⁵ Square, "Pricing"